Energy storage installations rise 61% this year

Battery makers and cell manufacturers have faced a tough 2024 thus far, with falling margins and revenues due to slower-than-expected worldwide sales of electric vehicles (EVs), reducing volumes.

However, BloombergNEF (BNEF) reports that the stationary storage market has risen 61%, and prices for turnkey systems are down 43% from 2023, which is part of driving that deployment. In April, the figure was a record low of $115 per kilowatt-hour for two-hour energy storage systems.

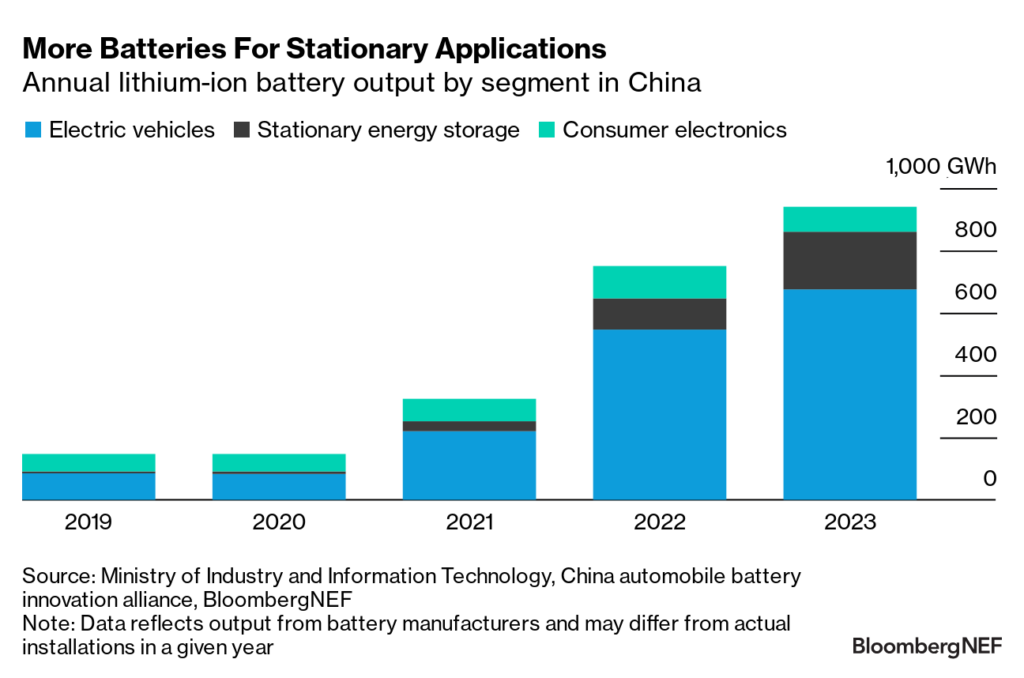

By looking at the annual lithium-ion battery output from Chinese manufacturers and assigning them an application, stationary energy storage overtook consumer electronics as the second-largest application for battery production. The global stationary energy storage market almost tripled in 2023.

Even combined, both were a long distance behind EVs. However, BNEF points out that the ratio of EV battery demand to stationary battery demand has fallen from 15-to-1 to 6-to-1 over the last four years:

Growth in the segment is much faster than EV battery growth, though, from a smaller base, and forecasted demand shows the segment continues to grow rapidly. That’s partly due to mandates in China for co-location with solar and wind for storage, plus the US Inflation Reduction Act, and measures rolling out in Europe, Japan, and Latin America, among others. Germany and Italy lead the residential market.

Regarding chemistry, BNEF expects NMC to hold a market share of only around 1% by 2030, as cheaper and potentially safer LFP chemistry takes market share.

Strong growth in energy shifting vs ancillary services

Early battery energy storage (BESS) projects often sold ancillary services into the grid, providing voltage support and preventing frequency droop, making considerable revenue for operators. However, as BNEF reports, the small markets for those services have largely been played out.

That has led to a strong growth trend in energy-shifting applications for BESS. The report points out that in China, some provinces require pairing solar projects with energy storage. The BNEF 2024 forecast compared to 2023 shows growth, to reach around 70% of all demand.

Supply drop, demand growth?

Future demand will depend heavily on whether the EV market and its associated battery demand can recover and the price of raw materials such as lithium carbonate, which continues to languish at relatively low spot prices, down some 80% from 2022’s peaks.

In terms of supply, the low prices are seeing miners and refiners react by stopping planned investments or mothballing assets.

Chemical company Abermarle recently placed its $1.3 billion lithium refinery in South Carolina on hold, with Albemarle CEO Kent Masters reportedly telling CNBC, “It’s difficult to justify investment projects where the prices are today.”

Australian lithium players have placed expansion plans on hold or closed mines throughout 2024, while Arcadium Lithium this week said it intends to “pause current investment in two of its four expansion projects”.

On an earnings call on August 6, CEO Paul Graves said, “It’s increasingly clear that at current lithium market prices, our industry cannot invest in capacity expansion at the pace announced to date.”